By Atty. Alvin Abenojar, LCB

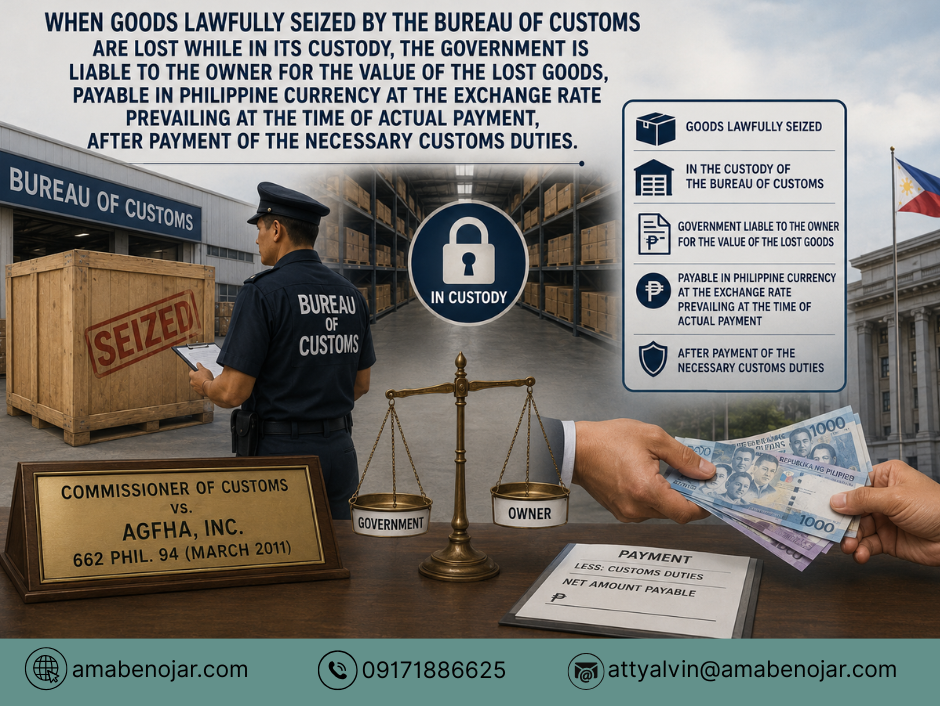

“When goods lawfully seized by the Bureau of Customs, and such seizure order is being challenged, the goods are lost while under Customs custody, the government is liable to the owner for the value of the lost goods, payable in Philippine currency at the exchange rate (ER) prevailing at the time of actual payment, after payment of the necessary customs duties and taxes. Further, the doctrine of state immunity does not apply in cases where the loss is due to the gross negligence or fault of government officials, as the State cannot use its immunity to perpetrate injustice.”

These are the doctrines laid down by the court in the case of Commissioner of Customs vs. AGFHA Incorporated[1] through the illuminating pen of Associate Justice Jose Catral Mendoza.

The crux of the case is whether or not the BOC is liable for the lost goods under its custody, and whether such claimed against the government violates state immunity.

The relevant portion of the case is wisely set out as follows: a shipment of textile clothing arrived at the Manila International Container Port and was held by the Commissioner of Customs on the grounds that the consignee was allegedly fictitious. Respondent AGFHA claimed ownership and intervened. After seizure and forfeiture proceedings, the District Collector of Customs ordered forfeiture of the shipment in favor of the government, a decision affirmed by the Commissioner. AGFHA appealed to the CTA. The CTA reversed the forfeiture and ordered the immediate release of the shipment to AGFHA, a decision that became final and executory after the Supreme Court denied the Commissioner’s appeals. Despite a writ of execution, the shipment could not be released because it was lost while in the Bureau of Customs’ custody, and the Commissioner could not account for its whereabouts. AGFHA sought indemnity for the value of the lost shipment, and the CTA ruled in its favor, ordering the Bureau of Customs to pay US$160,348.08, subject to payment of customs duties and taxes, computed at the exchange rate in effect at the time of actual payment.

Petitioner Bureau of Customs proffered the following arguments that AGFHA is entitled to recover only the acquisition cost of the lost shipment at the time of importation, not at the time of payment. Apropos to the first argument, it also contended that satisfaction of AGFHA’s claim constitutes a suit against the State, which requires filing a money claim with the Commission on Audit (COA) under P.D. No. 1445. The Commissioner also asserted that proceeds from the sale of forfeited goods must go to the general fund, and any payment to AGFHA would violate constitutional and statutory rules on government funds.

On the other hand, respondent AGFHA Incorporated advanced its argument that the applicable exchange rate should be the prevailing rate at the time of actual payment to preserve the real value of the lost shipment. AGFHA argued that the claim is not a money claim against the State but arises from a quasi-contract (solutio indebiti) under the Civil Code, and the State’s immunity cannot be invoked to avoid liability for its own unlawful acts. AGFHA also asserted that the government cannot invoke state immunity to perpetrate injustice, especially when the loss resulted from the Bureau of Customs’ negligence.

The High Court ruled in favor of AGFHA Incorporated, holding that the value of the lost shipment should be paid in Philippine currency at the exchange rate prevailing at the time of actual payment, in line with established jurisprudence in C.F. Sharp & Co. v. Northwest Airlines and Republic v. UNIMEX Micro-Electronics[2]. The Court also rejected the Commissioner’s argument that the claim is a suit against the State requiring COA approval, holding that the loss of the shipment was due to the Bureau of Customs’ gross negligence. Thus, the doctrine of state immunity does not apply. Astutely emphasized that the government cannot use its immunity to avoid liability for its own unlawful acts, especially when such acts result in manifest injustice. Further, the High Court emphasized that payment to AGFHA should be made after payment of the necessary customs duties and may be sourced from the proceeds of the sale of other seized or forfeited goods. Lastly, the CTA’s award of US$160,348.08 is upheld, subject to the conditions stated, and at the exchange rate prevailing at the time of actual payment. OoO